INSIGHT by Timothy Rahill, Jeroen van den Broek, ING THINK Economic and Financial Analysis

Despite little differential between green and grey at current spread levels, over the long-term, we expect ESG to outperform. ESG mutual fund inflows have been rising substantially, and we think the ECB targeting green will act as a driver.

| The European central bank president, Christine Lagarde has been clear; the fight against climate change is of utmost importance.

Yesterday, Lagarde stated that ECB’s green policy is now at the top of the agenda. Of course, as part of the ECB’s ‘strategic review’, the ECB will be looking into every avenue but their purchasing programmes are certainly a tool that can be utilised.

As it stands, there is very little structural outperformance for sustainable versus grey. There have been some cases of funding advantages in issuing green, and in times of volatility, sustainable spreads tend to be more sticky. However, in the long-term, we expect environmental, social, governance tilted bonds to outperform non-ESG with a structural difference and will trade tighter than grey bonds. This will offer a considerable cost advantage to green bond issuers.

Catalysts for outperformance in the long term:

〉ECB continually indicating the importance of green

The ECB has indicated the importance of sustainability and green bonds. Lagarde has now stated the ECB’s green policy is at the top of the agenda and bond purchasing could very well be the tool used. If ECB is to go further with targeting green bonds under their bond purchasing programmes (CSPP & PEPP), spreads will certainly price this in with tighter green bond spreads.

〉Substantial inflows into ESG mutual funds

In both EUR and USD, ESG mutual funds have seen considerably more inflows versus non-ESG mutual funds. The 1-year accumulated inflows amount to a much higher percentage of assets under management in ESG.

〉High demand for a limited yet growing pool of assets

As the green bond universe still remains limited, but with growing demand, there is high competition to invest. Currently, the Euro green bond supply has slowed slightly, maintaining the limited nature of green bonds. Furthermore, growing regulations for asset managers lead to additional disbalance between demand & supply.

| ECB is going green

There is little outperformance in ESG tilted spreads thus far, but we expect the spread differential to increase long term, as ESG tilted spreads begin to outperform grey and trade tighter. The ECB will play a role in this.

The ECB has indicated numerous times the importance of green and sustainable bonds. Now Lagarde has stated that the ECB will put sustainability at the forefront of their agenda and by the method of execution, they utilise their corporate bond purchasing programmes (CSPP & PEPP).

As it stands, the ECB holds 82 corporate green bonds under CSPP & PEPP, which accounts for 5% of the holdings (based on the number of corporate bonds). Although this is quite a considerable number in relation to the corporate green bond universe. Lagarde mentioned the ECB holds roughly 20% of the green bond universe (whole APP & PEPP). But looking directly at corporate purchases, the 82 green bonds held are roughly 45% of the eligible corporate green bond universe (180 bonds).

Of course, if the ECB add additional focus into green holdings, whereby they increasingly target green and sustainable bonds, ESG performance will soon follow.

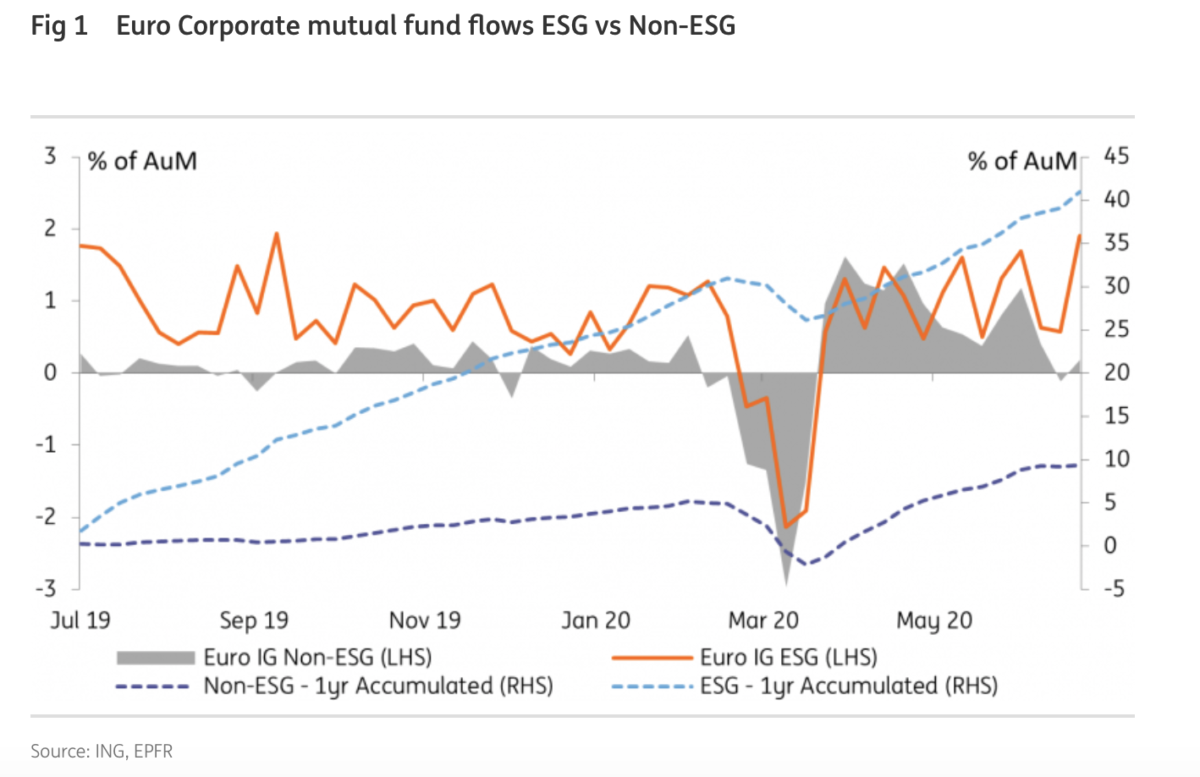

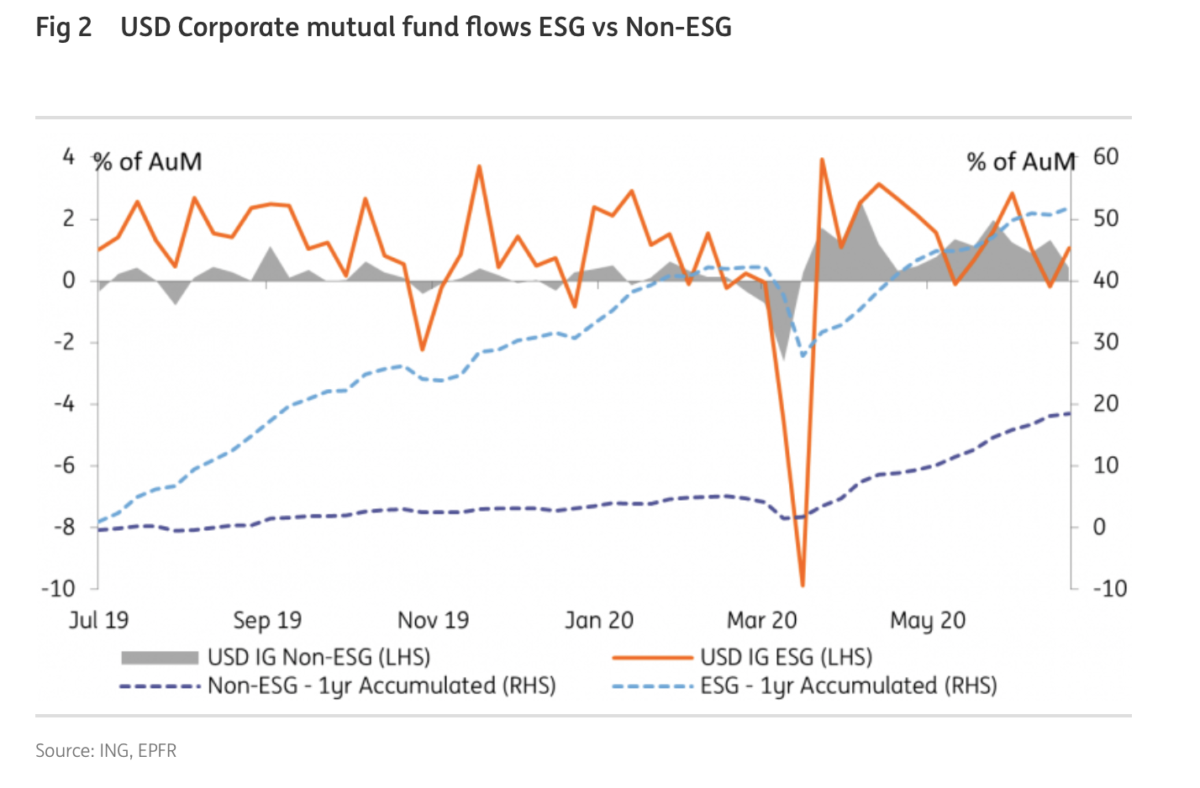

| Substantial inflows into ESG funds vs Non-ESG

Investment-grade ESG only mutual funds see considerably more inflows compared to non-ESG funds. In both EUR and USD investment grade mutual funds, ESG funds pencil in substantially more inflows in a percentage of assets under management basis (AuM).

As seen in Figures 1 and 2, over the span of the past 12 months, inflows have been very dominant for ESG funds. This is particularly the case in EUR, whereby apart from at the beginning of the crisis every week saw inflows. This has resulted in a considerable 1yr accumulation of inflows of just over 40% of assets under management, relative to the 10% inflows of assets under management seen in non-ESG funds.

USD ESG mutual fund flows have certainly been more volatile, and have dipped into outflows on occasion. Nonetheless, the 1-year accumulated inflows for ESG funds total just over 50% of AuM, compared to 18% of AuM in non-ESG funds.

As these inflows increase and the continuous growth in popularity for ESG, green bonds will certainly perform well compared to their grey bonds.

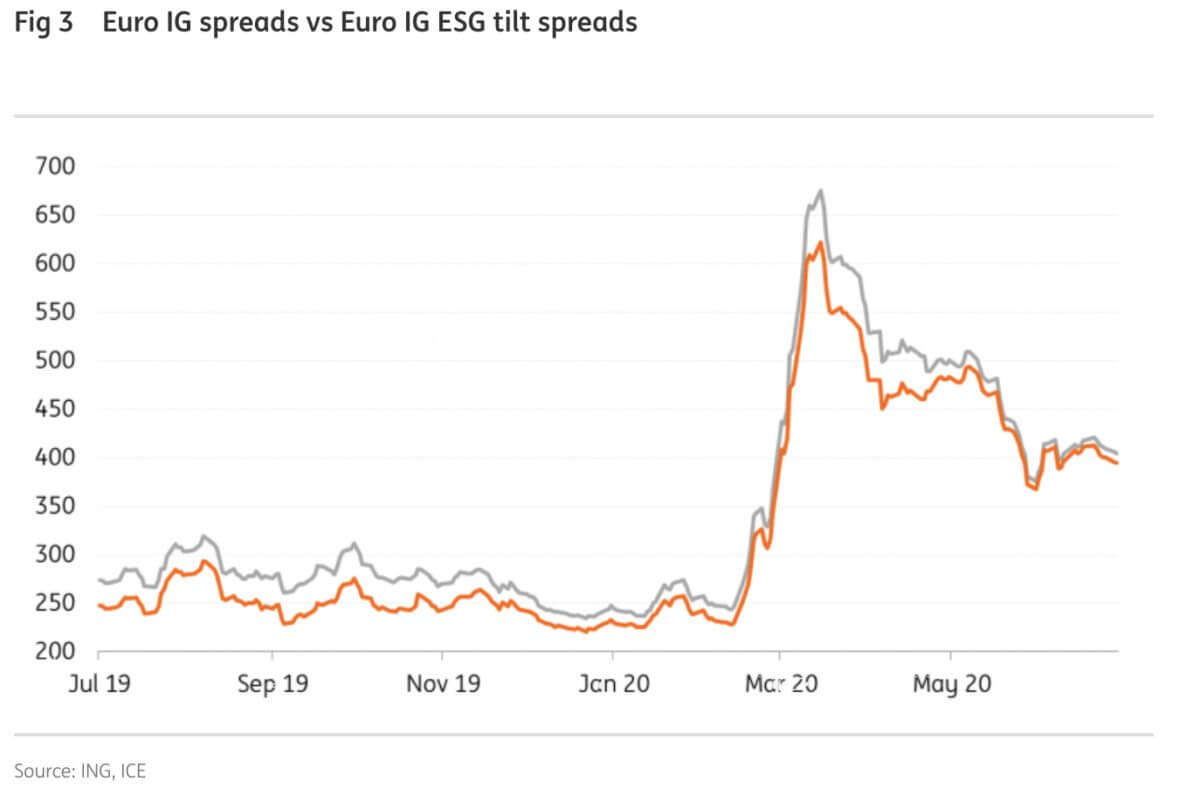

| No outperformance in ESG thus far

Despite the considerable inflows into ESG mutual funds, ASW spreads are not pricing in any outperformance for sustainable over grey. Thus far in most cases, sustainable tends to trade relatively in line with their grey curve, although this is name dependant. Indeed a number of utilities and industrials clearly benefit from tighter spreads on their sustainable issues, majority of others show a mixed bag, mostly falling in line with grey. Although, in the past there has been some moments of sustainable outperformance, particularly in volatile times, as spreads tend to be more sticky due to less flexible investors

As seen in Figure 3, which illustrates the ASW spread developments of a Euro investment grade index and a Euro investment grade index with an ESG tilt, they trade very much in line with each other, as the ESG tilt index remains within 1-7bp tighter than the overall index.

Although, the limited universe of ESG/green bonds will assist in the rally, as the growing demand for sustainability will have investors competing. Particularly as green bond supply is slowing slightly, yet demand is growing substantially, particularly with the ECB driving focus on green bonds. Supply of ESG remains limited due to many issuers not being seen as ESG worthy investments. Furthermore, the growing regulatory pressure on asset managers also leads to disbalance between demand and supply.

We expect sustainability to become more relevant in bond pricing and spreads, although only in the long term.

Indeed the ECB will truly drive the preference for ESG, alongside the increasing inflows into ESG tilted mutual funds. Despite the lack of outperformance structurally thus far, the growing demand will act as a catalyst in tightening, particularly as the disbalance between demand and supply continues.

We are bullish on sustainable over grey and believe a structural difference will develop as sustainable outperforms grey.

| This article was first published on July 9th, 2020 on ING’s THINK website at ING.com/THINK.

| All opinions expressed are those of the author. investESG.eu is an independent and neutral platform dedicated to generating debate around ESG investing topics.

| disclaimer

“THINK Outside” is a collection of specially commissioned content from third-party sources, such as economic think-tanks and academic institutions, that ING deems reliable and from non-research departments within ING. ING Bank N.V. (“ING”) uses these sources to expand the range of opinions you can find on the THINK website. Some of these sources are not the property of or managed by ING, and therefore ING cannot always guarantee the correctness, completeness, actuality and quality of such sources, nor the availability at any given time of the data and information provided, and ING cannot accept any liability in this respect, insofar as this is permissible pursuant to the applicable laws and regulations. This publication does not necessarily reflect the ING house view. This publication has been prepared solely for information purposes without regard to any particular user’s investment objectives, financial situation, or means. The information in the publication is not an investment recommendation and it is not investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Reasonable care has been taken to ensure that this publication is not untrue or misleading when published, but ING does not represent that it is accurate or complete. ING does not accept any liability for any direct, indirect or consequential loss arising from any use of this publication. Unless otherwise stated, any views, forecasts, or estimates are solely those of the author(s), as of the date of the publication and are subject to change without notice. The distribution of this publication may be restricted by law or regulation in different jurisdictions and persons into whose possession this publication comes should inform themselves about, and observe, such restrictions. Copyright and database rights protection exists in this report and it may not be reproduced, distributed or published by any person for any purpose without the prior express consent of ING. All rights are reserved. ING Bank N.V. is authorised by the Dutch Central Bank and supervised by the European Central Bank (ECB), the Dutch Central Bank (DNB) and the Dutch Authority for the Financial Markets (AFM). ING Bank N.V. is incorporated in the Netherlands (Trade Register no. 33031431 Amsterdam).