INSIGHT by Melissa Barbanell. This article was originally published by the World Resources Institute.

The past few years have seen ambitious, game-changing climate action from the United States. The Biden administration set a goal to cut greenhouse gas emissions in half by 2030 and reach net zero by 2050, and recent legislation — including the Inflation Reduction Act, Bipartisan Infrastructure Law, and a newly proposed EPA regulation to supercharge EV adoption — puts the U.S. within striking distance of its target.

But securing enough critical minerals to support a nationwide low-carbon transition poses a serious challenge.

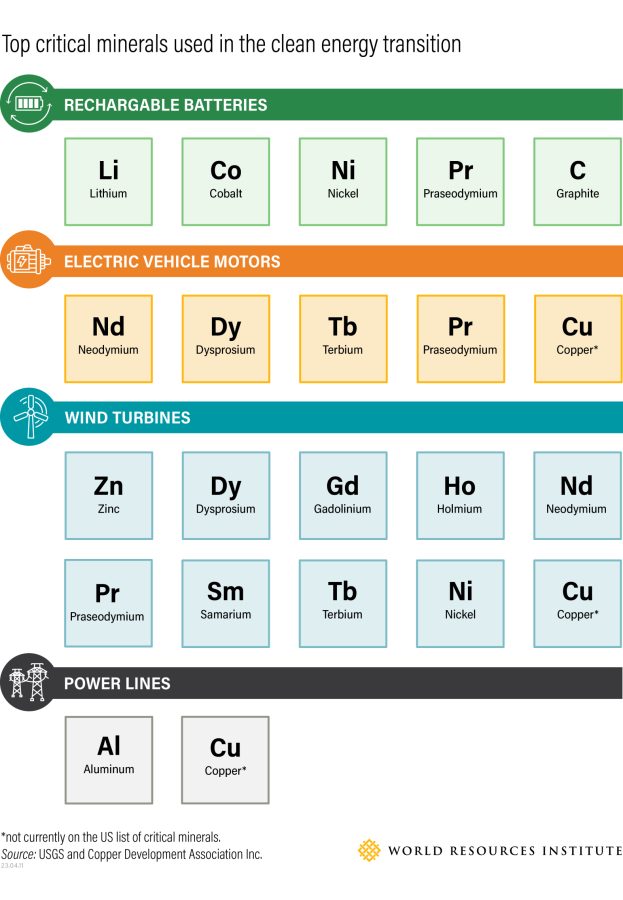

Critical minerals such as lithium, graphite, rare earth elements and cobalt are essential building blocks for a clean economy; they are used in wind turbines and solar panels, EV batteries and motors, renewable energy transmission and more. At present, the United States is reliant on imports for virtually all of these minerals. China controls the processing of key minerals and rare earth elements, which many see as a significant threat to the security of U.S. supply chains. And increased mining poses environmental and health risks both abroad and in the U.S., where many known critical mineral reserves are located in close proximity to Indigenous lands.

These issues have some stakeholders wondering if the supply of critical minerals could become a major bottleneck for the United States to achieve its climate goals. The U.S. must take action now to minimize these risks, secure its supply chains and drive responsible sourcing of critical minerals. Here’s what to know.

| What are critical minerals?

In the United States, critical minerals are those that are essential for U.S. national or economic security. These can be used in military equipment or in technology that will drive the economy, including clean energy components such as wind turbines, solar panels and EV batteries. To be considered “critical,” there must also be a risk that the country will not be able to obtain a mineral in the necessary quantities.

Of the 50 minerals included in the U.S. critical minerals list in 2022, at least 10 are essential to the clean technology transition:

〉Lithium

〉Cobalt

〉Nickel

〉Zinc

〉Aluminum

〉Neodymium

〉Praseodymium

〉Dysprosium

〉Terbium

〉Graphite

While copper is notably missing from the USGS list, in part due to significant U.S. copper reserves, other countries such as Canada do list copper as a critical mineral.

About Rare Earth Elements

Rare earth elements, or simply “rare earths,” are a family of 17 elements which, while relatively common, are found in very low concentrations and are difficult to extract. Four rare earth elements are particularly important to the clean energy sector: neodymium, praseodymium, dysprosium and terbium. These are used in permanent magnets for motors in wind turbines and electric vehicles.

| How much of these critical minerals will the U.S. need to meet climate goals?

A report by the International Energy Agency found that the availability of critical minerals will need to ramp up substantially to meet the goals of the Paris Agreement and avert some of the worst impacts of climate change. In order to build out enough clean technology to keep global temperature rise to 1.5-2 degrees C (2.7-3.6 degrees F), demand for nickel, cobalt and graphite is expected to grow by about 20 times while lithium demand is expected to grow to 40 times its current level. Demand for rare earth elements is expected to quadruple.

The scale of this global challenge will be felt in the United States as it uses the Inflation Reduction Act to increase clean technology development and uptake. The act includes numerous incentives to drive expansion of zero-carbon energy sources like wind and solar; production tax credits to support domestic manufacturing of these technologies; investment tax credits for zero-emission energy generation and storage facilities; incentives for Americans to decarbonize their homes through upgrades like heat pumps; tax credits for qualifying electric vehicles, and more.

Expanding renewable energy infrastructure in the U.S. and coupling it with stationary storage batteries will require significant quantities of critical minerals such as lithium, nickel and cobalt. Likewise, the rapid shift to electric vehicles will depend on new EV batteries that require these same minerals. As the country increases its overall reliance on electricity, moreover, it will require increased transmission which calls for large amounts of copper and aluminum.

| Where does the U.S. currently source critical minerals?

At present, the U.S. does not mine significant quantities of any of the relevant critical minerals needed for decarbonization. The country is 100% reliant on foreign imports for 12 critical minerals, including graphite, and greater than 50% reliant on imports for another 31 critical minerals, including rare earths (95%), cobalt (77%) and nickel (56%).

In the future (likely within 15-20 years), the U.S. will be able to rely on recycling as an alternative to mining for a significant portion of critical minerals. But in the short term (by 2030), there will not be sufficient quantities of these minerals in circulation to make recycling a feasible approach. Additionally, there are a range of research efforts underway to obtain the necessary minerals without mining virgin land, including recovery from coal waste or hard rock mine tailings. But, at present, the stage is set for a significant increase in the amount of mining and processing of these minerals globally.

| Does the inflation reduction act require critical minerals to be sourced domestically?

Yes, to some extent. The Inflation Reduction Act explicitly requires domestic sourcing of critical minerals only for its electric vehicle tax credits. Other clean energy technologies (such as wind and solar) do not need to use domestically sourced minerals to qualify for the Investment Tax Credit (ITC) or Production Tax Credit (PTC). However, the act offers an additional 10% bonus credit to incentivize companies to incorporate U.S.-sourced critical minerals in all types of clean energy components.

Critical minerals sourcing requirements for EV tax credits

To receive the full value of the Inflation Reduction Act’s Clean Vehicle Tax Credit (up to $7,500 for qualified purchases), a portion of the vehicle’s critical minerals must have been extracted or processed in the United States or in a country with which the U.S. has a free trade agreement. Critical minerals recycled in North America can also fulfill this requirement. Vehicles placed in service before January 1, 2024 must contain at least 40% domestically sourced critical minerals to qualify; this ratchets up yearly through 2027, after which the percentage required is 80%.

Meeting critical minerals requirements accounts for half the value of the Clean Vehicle Tax Credit. The other half requires that a certain percentage of the vehicle’s battery components were manufactured or assembled in North America. At present, batteries must contain at least 50% domestically manufactured or assembled components; after 2027, this increases to 90%.

In addition, starting in 2025 for critical minerals and 2024 for battery components, no vehicle will qualify for the EV tax credit if any of these materials were sourced from a “foreign entity of concern,” such as China.

There is one exception, which provides a path for commercial vehicles to receive the full amount of the EV credit without requiring any domestic content.

Critical minerals sourcing for other clean energy technologies

The Inflation Reduction Act also offers an Advanced Manufacturing Production Tax Credit (AMPTC) for companies which domestically manufacture and sell clean energy technology. The AMPTC is a per-unit tax credit equal to 10% of the cost of production for each clean energy component domestically produced and sold by a manufacturer.

Fifty different critical minerals are listed in the Inflation Reduction Act as eligible “clean energy components,” meaning companies can claim the AMPTC when producing these minerals in the United States. There is no phaseout for the tax credit’s application to the production of critical minerals.

| What challenges will the U.S. face in obtaining critical minerals?

As the U.S. evaluates how it can ensure a stable supply of critical minerals, it must grapple with a range of challenges. Two of the most difficult are that China controls the lion’s share of mineral processing capacity and that critical minerals mines have not, and cannot, live up to the desired zero-harm standard.

Supply chain vulnerability

The dominance of China in the critical minerals market is seen by some U.S. stakeholders as a significant threat to supply chains. While China corners the market in production of only two of these minerals, the processing situation is very different. China processes over 80% of all rare earth elements, over 60% of all cobalt, over 50% of all lithium and over 30% of all nickel.

Fear of supply chain risks is well-founded, as China has proved itself willing to wield this dominance as a political tool. For instance, in 2019, with the U.S.-China trade war intensifying, China threatened to cut off exports of rare earths to the United States. And in 2010, in retaliation for Japan’s holding of a Chinese fishing boat captain who was fishing in disputed waters, China did block exports of rare earths to Japan. These politically driven sales restrictions resulted in dramatic price spikes.

In considering how to address China’s dominance as well as the strictures of the Inflation Reduction Act, the U.S. should look for opportunities to support increased mining and processing facilities both domestically and in free trade agreement partner countries. The U.S. has free trade agreements with a few high-producing nations — including Australia, Chile and Peru — but oftentimes these nations still export to China for processing. Compared to mining, mineral processing has a smaller footprint with more manageable environmental risks, and processing facilities can be permitted and built more quickly.

Mining impacts

Mining, by its nature, is not a zero-harm activity. It poses significant risks to the environment and local communities, including air pollution, water depletion and pollution, and biodiversity loss.

Mining waste can also create significant risks; for example, improperly managed waste rock (overburden) can release acid mine drainage into the surrounding environment, and tailings impoundments (process waste) can sometimes leak and cause groundwater contamination. On occasion, catastrophic tailings dam failures occur, resulting in significant environmental harm and even loss of human life. Finally, there are social risks associated with mining, such as increased crime and gender-based violence.

In some cases, neighboring communities have been historically disenfranchised and not given the opportunity to participate in the licensing process. This can mean their objections and/or insights on how to best build projects or mitigate impacts may not have been sufficiently considered. Indigenous communities may be particularly vulnerable to the impacts of expanded critical minerals mining, as a significant portion of the mineral reserves needed for the U.S. energy transition are located within 35 miles of Native American reservations.

If everything goes right and if a mine is located in the ideal environment (for example, one with ample water and at low risk of flooding), impacts can in theory be localized to the mine site and avoid affecting nearby communities. In addition, mining companies may bring essential services to local communities in the form of health care, access to fresh water and well-paying jobs.

The challenge is that given the footprint of a mining operation, the time period over which mines operate (on the order of decades), and the fact that mines must often be managed in perpetuity, it is difficult to have everything go right. Laws and permitting must be sufficiently protective and enforced; environmental impact studies must be carried out and address all relevant risks; changes in the ore body composition must be noted and addressed quickly in case it shifts toward a significantly higher percentage of a dangerous element; effective management systems must be in place; and there must be no accidents, such as liner failures, air pollution control device breakdowns or wildlife incursions.

As global demand for critical minerals grows, effective regulation and responsible corporate practices must minimize environmental degradation, avoid environmental injustice and address the social risks associated with mining — including providing local communities with a forum to have voice in the process.

| How can the U.S. responsibly source enough critical minerals to meet climate goals?

There is widespread agreement that additional mining of critical minerals is necessary in the short- to medium-term to support a clean energy economy. Estimates suggest that more than 300 new mines will be needed globally to meet demand for EV batteries alone.

Responsibly increasing mining in the U.S. to the extent possible, and fostering responsible practices abroad, will help ensure that this additional mining is done under the most rigorous standards available. The Inflation Reduction Act’s critical minerals sourcing requirements directly support both goals by incentivizing domestic production and helping shore up trading relationships with like-minded allies.

Encourage domestic production and address U.S. mining challenges

Producing critical minerals domestically allows the U.S. to ensure high standards are in place governing mining operations and helps meet the administration’s dual goals of creating good-paying American jobs and addressing the climate crisis. In addition, electric vehicles with critical minerals mined in the U.S. can qualify for the Inflation Reduction Act’s Clean Vehicle tax credits; in this way, domestic mining will help encourage uptake of electric vehicles within the U.S.

Almost every new mine in the United States will be required to go through review under the National Environmental Policy Act (NEPA), including developing Environmental Impact Statements which consider the cumulative impacts on everything from biodiversity to climate change. The U.S. also has a network of strong environmental laws — including the Clean Air Act, the Clean Water Act, and the Resource Conservation and Recovery Act — which govern every aspect of a mine’s operation, require permits to be granted and provide for state regulator oversight of operations. Finally, domestic mines are subject to financial assurance requirements to provide a clean-up fund if the operation does cause environmental harm.

It is important to note that these regulatory and statutory safeguards cannot always address all potential issues. There may be unintended consequences of mining, such as groundwater contamination from tailings dam liner leakage or pit lakes formed after closure. This is why the U.S. and the industry must focus on continuous improvement and consider new and novel mining opportunities which could minimize risks as they work to increase critical minerals mining capacity.

Expanding domestic mining will also require overcoming the permitting and litigation hurdles associated with developing new mines. This is no small feat, as new mines in the United States take, on average, a decade to go through the NEPA process and can be embroiled in litigation under NEPA for upwards of 20 additional years. Efforts are underway to pass permitting reform legislation; in the meantime, increasing funding to the agencies that oversee NEPA compliance and encouraging concurrent reviews among all agencies involved — which may include multiple federal agencies along with state, tribal and local agencies — could help speed this process.

Finally, the Biden administration’s support for mining is seen as mixed; on the one hand, it issued a 20-year moratorium on mining in northern Minnesota and designated the Avi Kwa Ame National Monument in Nevada, which may disallow mining where rare earth projects have been proposed. On the other hand, it is supporting direct lithium mining in California’s Imperial Valley and has distributed millions of dollars in support of rare earth and lithium projects over the last two years.

Support U.S. and major mining companies operating abroad to improve performance

Because the U.S. does not have sufficient critical minerals reserves to meet its own needs — and because it can take over a decade to bring new domestic mines into production — the country must continue to rely at least partially on imports. To help ensure these imports are responsibly sourced, companies from the U.S. and other developed nations should be encouraged to operate mines abroad. Companies that are publicly traded on major exchanges are subject to higher levels of oversight and are more likely to perform responsibly than smaller companies.

The Minerals Security Partnership (MSP) aims to bolster global critical minerals supply, in part by supporting partner countries’ companies in developing mining, processing and recycling in compliance with the highest environmental, social and governance standards. The partnership comprises 13 members including the U.S., Canada, Australia, several European countries, the European Commission, Korea and Japan. The countries are looking at projects that can be delivered by their companies around the world; they hope to settle on approximately 12-15 investments globally that will address all aspects of the industry, from mining to midstream processing to battery manufacturing. The MSP includes guiding ESG principles to ensure higher standards, greater transparency and local benefits.

While the MSP provides a means of government financing and therefore some protection for companies investing abroad, this will only address a small share of needed supply chains. It is still necessary to mitigate the political challenge of operating in unstable developing countries, where nationalization of assets is a serious risk.

Investor-state dispute settlement (ISDS) provisions were designed to provide a neutral and impartial process to resolve conflicts between countries and foreign investors. However, over 200 U.S. lawyers and economists have expressed concern that ISDSs erode national sovereignty and give corporations “alarming power” to override domestic legislation. European opponents have also argued that ISDSs may deter national authorities from passing laws to protect the environment, health and safety. The Office of the United States Trade Representative should consider offering scaled-back ISDS provisions to address situations where assets have been or are threatened to be expropriated outright and requiring investors to exhaust local courts first — similar to how the United States-Mexico-Canada Agreement adjusted its ISDS provisions in 2020.

Help develop responsible international mining standards

The U.S can also champion responsible mining abroad by helping develop a unified approach to determining the environmental and social performance of critical minerals mines.

A wide range of assurance protocols currently exists to regulate the ESG performance of the mining industry. Some standards were created through multi-stakeholder processes, some were developed by the mining industry to self-regulate, some were developed at the behest of the purchasers of mineral products, and others were developed through multilateral government engagement. These cover a range of different subject areas and may or may not require outside assurance. This proliferation of international initiatives increases the risk of duplication and inconsistency.

Industry Standards Make an Impact

A 2020 UN Environment Programme report identified environmental challenges posed by mining operations in Key Biodiversity Areas and protected areas, including 33 World Heritage sites, and called for new governance guidelines in line with 2030 Sustainable Development Goals. In response, the 26 member companies of the International Council on Mining and Metals have committed to neither explore nor mine in World Heritage Sites and to respect all legally protected areas.

There has been ongoing work to harmonize these standards and simplify comparison. The United States and the MSP should consider supporting these efforts by building a more comprehensive understanding of the value of different assurance protocols and offering a transparent analysis of them. They must also recognize that there will not be a one-size-fits-all solution, given the wide variety of national and local circumstances governing mining operations. For example, the Fair Cobalt Alliance, which supports responsible mining in the Democratic Republic of the Congo, advocates for progressive standards based on continuous improvement. Such standards could consider the proliferation of artisanal and small-scale mining in the country and the poverty cycle which drives this activity.

Vehicles like the MSP Principles for Responsible Critical Mineral Supply Chains and the U.S. Memorandum of Understanding with Zambia and the Democratic Republic of the Congo should offer a range of options that such local circumstances into consideration. Appropriately, the MSP’s Guiding Principles did not endorse a single ESG accreditation framework, recognizing that there are many standards which are continuing to develop.

Another challenge to evaluating responsible sourcing is the traceability of minerals. It may prove impossible to show that an end product uses critical minerals sourced from a particular mine — however, efforts are underway within the battery sector to do just that.

| As demand for critical minerals grows, the U.S. must drive continuous improvement and responsible mining

As the United States’ need for critical minerals escalates, it is important to remember that this is not a zero-sum game. The country must not only pursue a rapid switch to greener energy, but do so responsibly to ensure the transition is just and equitable.

The U.S. can increase mining for critical minerals while establishing guard rails to mitigate social and environmental impacts wherever possible. As the nation and manufacturers decide where to import minerals from, they should consider the following factors to help determine what constitutes a responsibly sourced supply of critical minerals:

〉The regulatory framework under which mining is taking place. Purchasers should be confident that compliance with and enforcement of strong environmental laws and regulations are part and parcel of operating mining, smelting and refining operations.

〉The existence of forums for neighboring communities to express their concerns and have a voice in the process.

〉The environmental and social track record of companies seeking to operate mines and from which U.S. companies are purchasing materials.

〉The transparency of mining companies in terms of performance reporting; for example, whether they report against an external assurance protocol and whether that reporting is third-party assured.

〉The process that critical minerals must take to come to market. Even if materials are mined in a country that does not create supply chain risks, purchasers must evaluate where the refining and processing of those minerals takes place and the environmental performance of the processing facility.

〉Whether the mining of minerals maximizes benefits to local communities. Purchasers must consider whether mining is an extraction-only relationship or if there is an opportunity to increase wealth and knowledge on a longer-term basis.

This is an extraordinarily complex and challenging set of issues to address, but the potential upside is enormous.

Critical minerals mining presents an opportunity to halt the unsustainable culture of fossil fuels. Whereas fossil extraction and burning will result in continuously rising greenhouse gas emissions, increased mining of critical minerals will ultimately set the stage for a clean circular economy wherein recycling and reuse of these materials becomes the norm.

By supporting new mining operations domestically and encouraging sustainable practices abroad, the United States can help mitigate the negative environmental and social costs while maximizing the economic and climate benefits of these critical minerals.

| All opinions expressed are those of the author and/or quoted sources. investESG.eu is an independent and neutral platform dedicated to generating debate around ESG investing topics.